我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

Please update your browser.

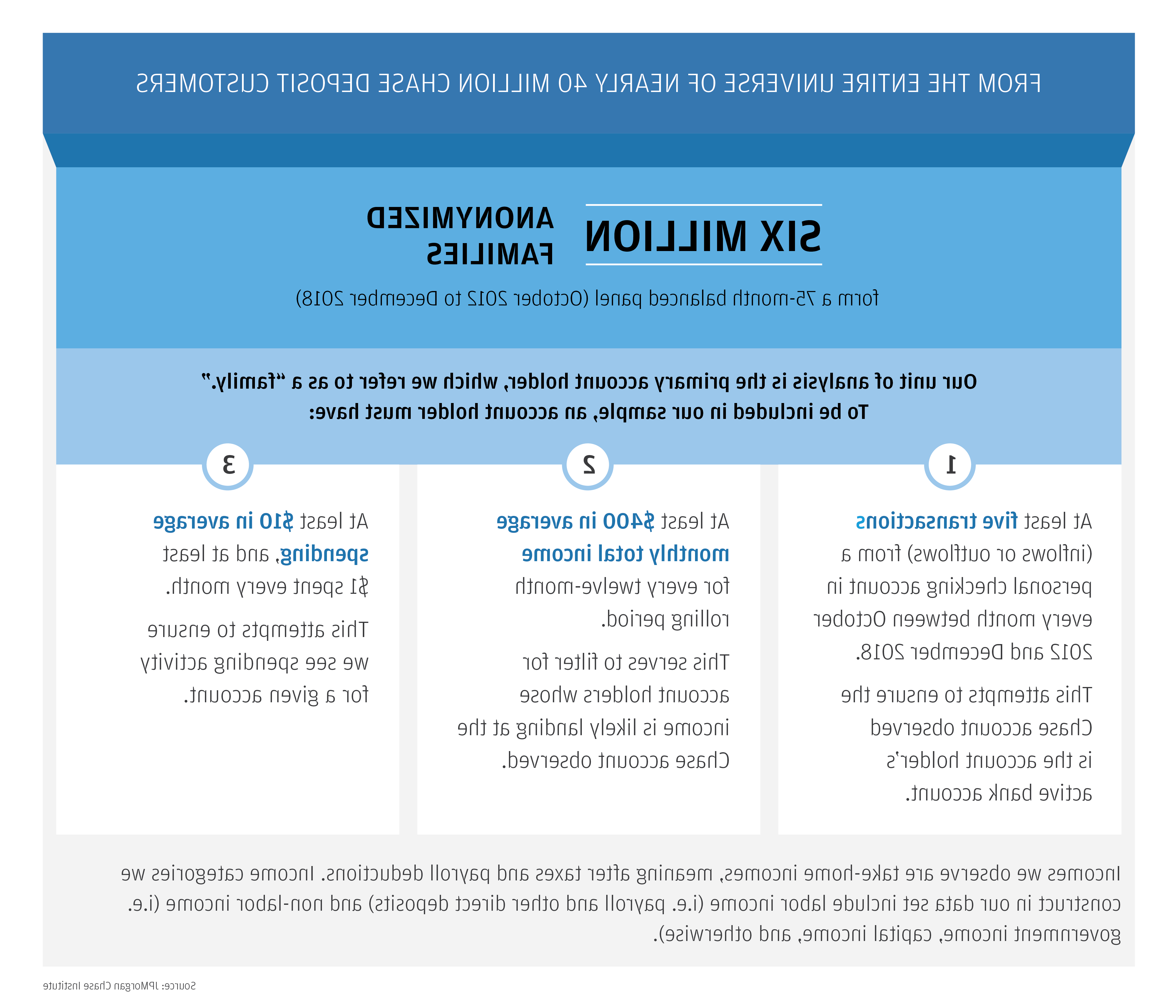

In this report, the JPMorgan Chase Institute uses administrative bank account data to measure income and spending volatility and the minimum levels of cash buffer families need to weather adverse income and spending shocks.

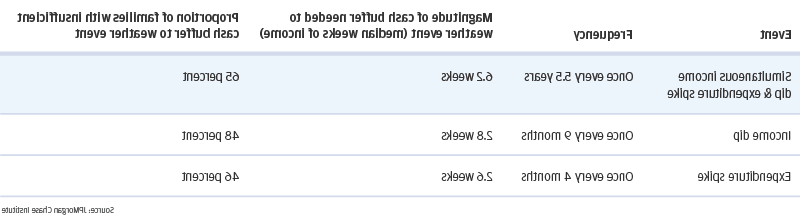

Inconsistent or unpredictable swings in families’ income and expenses make it difficult to plan spending, pay down debt, 或者决定存多少钱. Managing these swings, or volatility, is increasingly acknowledged as an important component of American families’ financial security. 在之前的澳博官方网站app研究所(JPMCI)研究中, we have documented the high levels of income and expense volatility families experience. In this report, we make further progress toward understanding how volatility affects families and what levels of cash buffer they need to weather adverse income and spending shocks. 我们探讨了六个关键问题:

Our findings have important implications for designing savings strategies to improve families’ financial health and resilience. They suggest that the tools currently available to help families weather volatile income and spending could be better tailored to an individual’s cash flows. Simply saving a certain percentage of monthly income may leave a family with an inadequate cash buffer, exacerbating financial distress in cash flow negative months and resulting in under-saving during cash flow positive months. Instead, families may need to more aggressively harvest savings opportunities during income spike months. 我们为家庭提供经验指导, financial health advocates, financial advisors, and policymakers on the minimum levels of cash buffer families need to weather adverse shocks. 鉴于稳定对家庭财务生活的健康起着关键作用, it is critical that we continue to gauge how income and spending volatility are changing for American families and the implications for families’ financial health.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. 不负责(也不提供)任何产品, 该第三方网站或应用程序的服务或内容, 明确带有澳博官方网站app字样的产品和服务除外 & Co.